Product Explore - Money Market ETFs

Written by Exvestigate on July 21, 2025

TL;DR

If you’re holding cash in a broker account like Saxo and earning little to no interest, EUR-denominated money market ETFs like Amundi Smart Overnight Return UCITS ETF or Xtrackers II EUR Overnight Rate Swap UCITS ETF may offer a low-risk, liquid alternative with better returns. While not risk-free (e.g., no deposit guarantee and swap-based structure), these products can help you recover lost interest on amounts like €10,000, especially when traditional banks underperform.

What is the problem to solve?

One of my brokers is Saxo. Saxo does pay interest on the cash you have in your investment account which is wonderful. However:

- Interest is only paid when your cash balance exceeds €100,000 (!).

- The interest rates on EUR cash are very, very modest. The word “puny” comes to mind.

On average I have around €10.000 in cash, never less then €8.000. So, I lose around €160 per year compared to 2.0% savings account. Nothing dramatic, but I would still like to have that money.

I could transfer cash from my Saxo account to a regular savings account and move it back when needed. But that’s a bit of a hassle, and my main street banks also offer meager rates: around 1.25% to 1.50%. Fixed-term deposits are not an option, as I may need access to the funds on short notice.

This is why I started looking into money market funds (MMFs). These are low-risk, investment-like vehicles that typically offer higher returns than standard bank accounts. The trade-off? MMFs are not covered by the European Deposit Guarantee Scheme (DGS), which protects up to €100,000 in bank deposits. Still, for modestly higher returns, they may be worth considering.

Are there products that could help me get my precious €160?

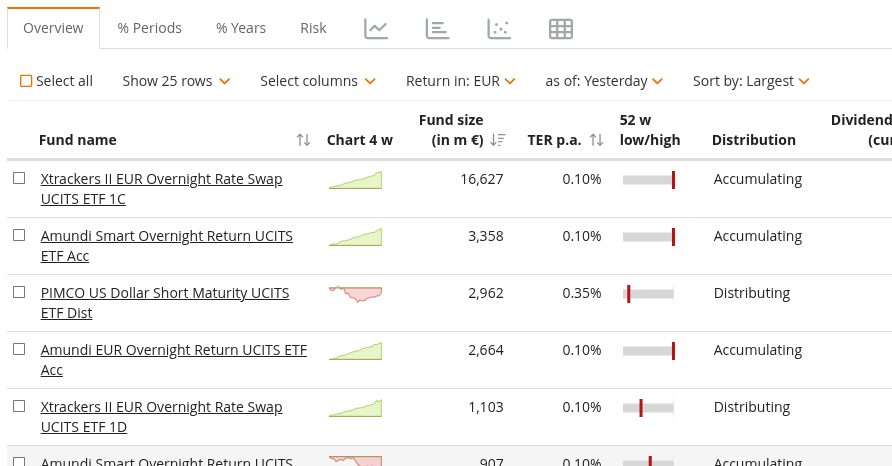

Available ETFs

As often I start with justETF to see what MMFs are available in the form of ETFs. The ETF-screener shows 27 products in the asset class Money Market. I sorted them by fund size and reviewed their attributes. You should see a table like this one:

To see it live in JustETF go here.

Now, what are my criteria?

- I need a fund that has EUR as the fund currency. Why? Because currency risk is a real thing. In the first half of 2025 the USD lost over 12% to the EUR. Imagine your savings losing 12% of their value. You can also look for currency hedged products, but currency hedging isn’t free. Especially if interest rates are higher in the currency being hedged. Which is applicable for the USD in case you were wondering.

- Fund size matters. Larger funds tend to be more efficient and resilient.

- Low Total Expense Ratio (TER). Margins are already thin; fees must be minimal.

- Should track a well-known benchmark.

- The risk indicator in the Key Information Document (KID) must be 1. For me, only the lowest risk class is acceptable in this case and makes it look more like an actual savings account.

- My preference is to have an MMF that is distributing rather than accumulating.

Two MMFs seem interesting to investigate further:

Another ETF that shows up in the selection is iShares EUR Government Bond 0-3 Month UCITS ETF EUR (Dist). This ETF was rejected due to its small fund size of around €7M and different index tracking approach (treasury bills, not interest rates). Although the risk indicator is 1 and the TER is low (0.07% - May 2025 Factsheet), this ETF is not quite what I am looking for.

Let´s take a closer look at the two selected ETFs.

Product Comparison

The compare-feature in justETF is a good start but I will always look at the product pages from the asset managers themselves.

Both products are fulfilling my criteria and are highly comparable but there are some notable differences. I will refer to the products as Xtrackers and Amundi to keep this section a bit more readable.

- Over 3 years Amundi did +3.04% per year and Xtrackers +2.97%. This small difference seems to be consistent. Current YTD are +1.49% for Amundi and +1.31% for Xtrackers.

- The Risk-Return chart indicates that Amundi is a bit more volatile than Xtrackers. This is the case over most time periods that can be selected. Both are still very low risk.

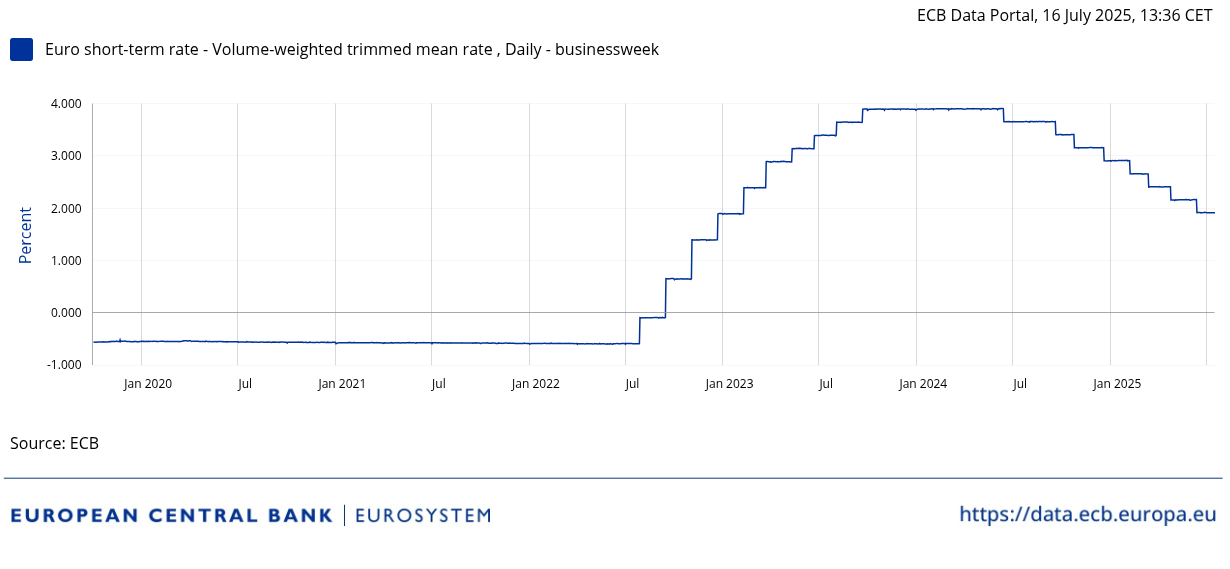

- Amundi follows the €STR Compounded Index. Xtrackers the Solactive €STR +8.5 Daily Total Return Index by Germany-based index provider Solactive. The main difference is that Amundi’s index calculates the interest on both the initial principal and the accumulated interest from previous days; Xtrackers uses simply the risk-free overnight interest rate + 8.5 bps.€STR and compounded €STR are both published by the ECB. NB. These rates are published by the ECB but not set by the ECB. They are “reflecting trading activity” so the market set these rates.

- Amundi distributes annually, Xtrackers quarterly.

A good point to note is that the returns for these funds can be negative when interest rates are negative. Anyone remember 2021? A logical consequence of following a benchmark but still. Naive me thought you just stopped your activities to avoid getting negative returns but that is not how these funds operate. They just follow the benchmark.

Both MMF’s list “Indirect Replication (Swap)” as their replication method. How does that work?

Indirect Replication? SWAPS?

Let´s take a popular ETF like iShares Core S&P 500 UCITS ETF USD (Acc). Its replication method is “Physical (Full replication)” which is exactly what you think it is. This means the ETF buys and holds every stock in the S&P 500 it tracks, in the same exact weights as the index. So, if I buy €1.000 of this ETF, the ETF buys a bit of NVIDIA, Google. Apple etc. for each of the 500 stocks in the S&P 500.

Swaps are a form of synthetic replication and this works very differently. The two ETFs we look at do have assets, very liquid ones. When I invest, they buy more of these assets. As you would expect, these assets generate a return. The funds make an agreement with a counterparty to exchange this return for their benchmark. So, Xtrackers would exchange their return for €STR +8.5 with a counterparty. This is a total return swap.

In this case, Xtrackers gets a predicable return, so it generates its benchmark, and the counterparty gets a variable one i.e. the fund’s actual return. Please note, you only exchange returns and not collateral.

If you think swap-based ETFs are more complex than ETFs that use physical replication, you would be right. But there are plenty of checks and balances in place and this is a much-used strategy. The complexity is not a problem. However, you do get a bit more risk because a counterparty is involved and counterparties might go bankrupt or refuse to pay.

Counterparty risk exists but is minimized by using top-tier institutions:

- Xtrackers: Barclays, Deutsche Bank, Goldman Sachs, J.P. Morgan, Société Générale

- Amundi: Société Générale, Crédit Agricole, BNP Paribas, J.P. Morgan

In short, the ETF holds safe, liquid assets, but it swaps the return of those assets for the benchmark return (like €STR). This means you get the performance of the benchmark, but with some added complexity and a small counterparty risk.

Takeaway

After reviewing these options, I’m confident both Amundi and Xtrackers are reasonable alternatives to parking cash in low-interest bank accounts. I will definitely use one of them for my Saxo-account.

If you don’t have a strong preference, Amundi offers slightly better returns over multiple time frames, albeit with marginally higher volatility.

One caveat: transaction costs. Buying or selling €5,000 of either ETF on Saxo costs me around €3. Sometimes, Saxo offers commission credits, so that may be waived. Even if I spent €10 here and there, turning my “lost” €160 into €150 is still worth it.

As the saying goes: “If you can’t manage the small things, you can’t be trusted with the big ones”.